Luxury is Back. LVMH isn’t

The global personal luxury goods market, valued at €358 billion, may grow by 3–5% as early as this year after stagnating in 2025, according to a report by Bain & Company. Similar expectations are also shared by HSBC. Geographically, the United States remains the main growth driver, while Europe and Japan are also seeing resilient domestic demand, and finally, China, where the market continues to anticipate a recovery.

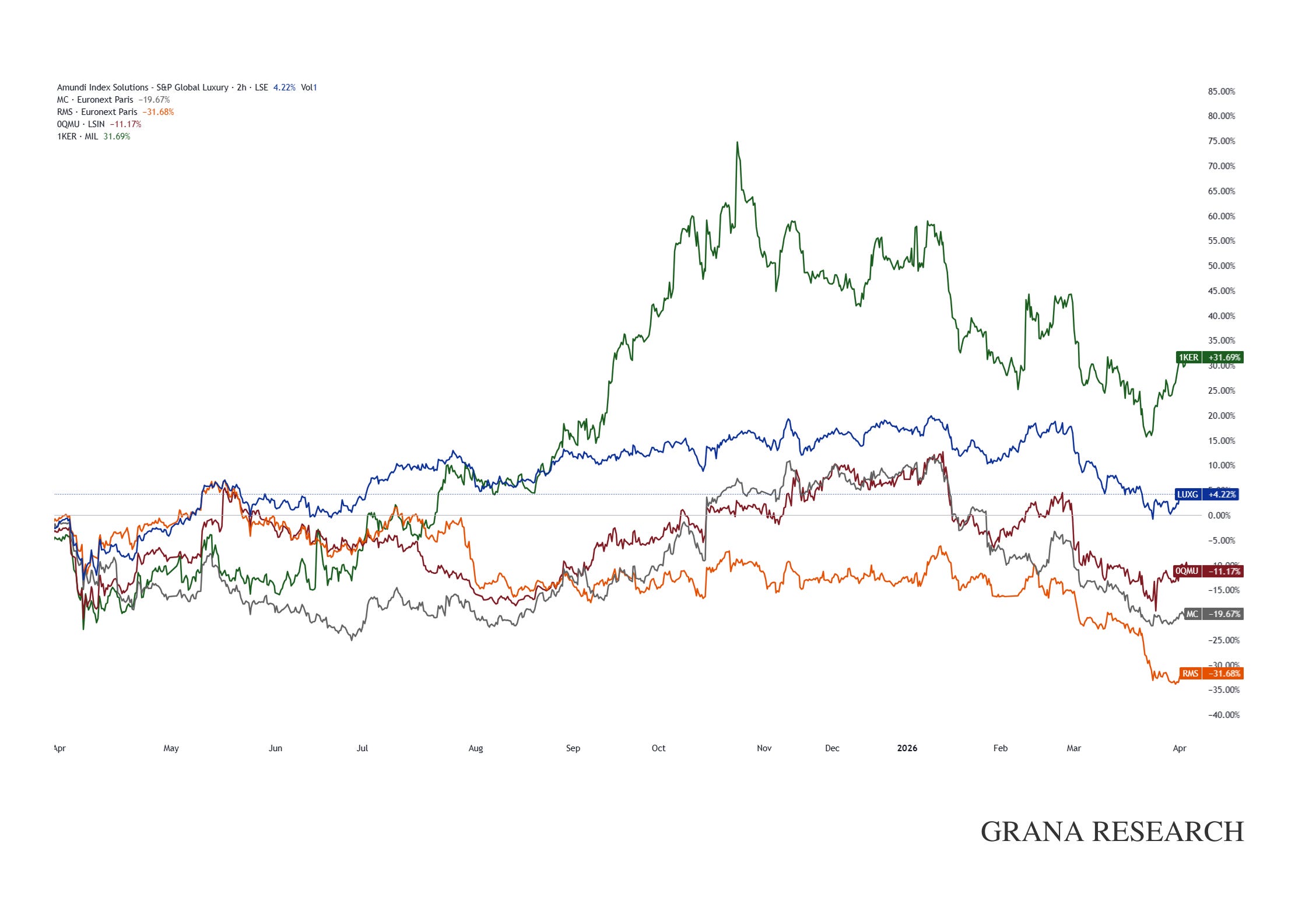

Against this backdrop, the performance of LVMH Moët Hennessy ($LVMH, $MC.FP) shares appears almost paradoxical: the largest company in the sector would seemingly be among the primary beneficiaries and grow at least in line with the market, yet over the past three years it has consistently lagged behind its peers, while also dragging down the entire thematic benchmark. One of the most common explanations, widely cited by the sell-side, is the company’s active M&A activity, which, among other factors, contributes to an increased “conglomerate discount.”

Analysts, including Morgan Stanley, UBS, and HSBC, described both the latest annual report and the previous one as “mixed but encouraging” in their post-earnings reviews. At JP Morgan, the negative impact of large M&A transactions is highlighted as one of the key risks that could lead to a downgrade of the “Neutral” rating and target price.

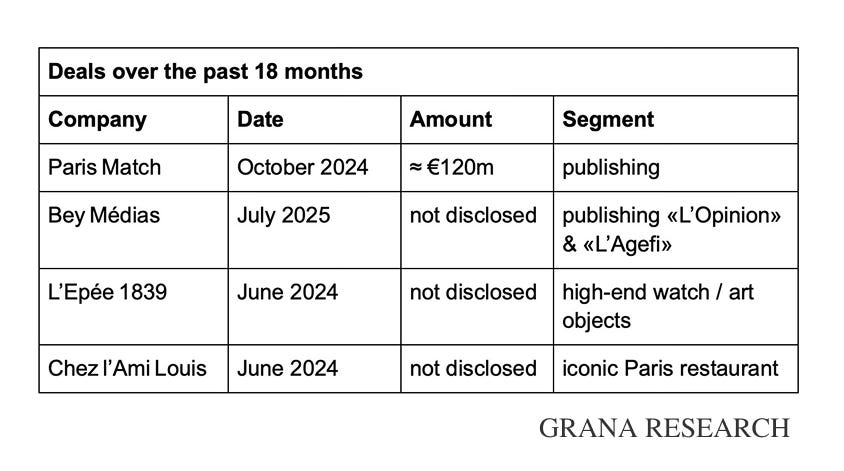

To be fair, deals on the scale of Tiffany, valued at $15.8 billion, are relatively rare. Over the past year, the company has focused less on large-scale portfolio expansion and more on strengthening the ecosystem around its core brands (Louis Vuitton, Dior, etc.), occasionally opening a window into media, gastronomy, and lifestyle. These efforts are aimed at increasing customer engagement. Accordingly, the downside risk discussed on Wall Street is not tied to a one-off financial impact from such transactions, but rather to a gradual compression of operating margins if the number of such non-core acquisitions increases — particularly in a scenario where the core business slows.

However, it appears that such deals will continue. During the Q3 2025 earnings call, management emphasized that these initiatives help drive traffic and create an emotional connection between the customer and the brand.

Frankly, it has long been difficult to classify LVMH Moët Hennessy unequivocally and without reservations as “hard luxury” — unlike Hermès ($RMS.FP), which relies on a narrow but highly loyal client base, tightly controls supply (going as far as legal disputes over the right not to sell its exclusive $15,000 handbags to insufficiently loyal customers), and maintains strong pricing power. While LVMH is trying to strengthen “brand connection” through ventures like bakeries, Hermès bags continue to fly off the shelves like hot cakes. According to Sotheby’s, their average resale price increased by around 35% year-on-year, while demand from collectors remains strong: sales of Birkin and Kelly bags rose by 44% in 2025 compared to 2024 and by 55% relative to 2023.

Therefore, beyond M&A activity, LVMH has already accumulated a whole set of challenges: limited room for further price increases, risks of brand dilution, frequent turnover of creative directors, and increasingly visible signs of succession tensions. We discuss these in more detail below.

Louis Vuitton Has Run Out of Price Hikes

Remember the “shut up and take my money” meme? Until recently, it fairly accurately described the behavior of luxury consumers. Now the tone is shifting: an uncomfortable question is increasingly being asked — what exactly am I paying for?

The personal luxury market is facing the consequences of years of price increases, which have led to the loss of “aspirational” demand and a weakening of interest from younger consumers, including Generation Z, in favor of so-called affordable luxury. The number of customers has declined from 400 million in 2022 to around 340 million in 2025, and could shrink by another 20–30 million. Notably, even the wealthiest clients — who account for roughly 46–47% of the market — have started to spend less. The contraction of the customer base and the cooling of key buyers are setting a more subdued trajectory for financial growth.

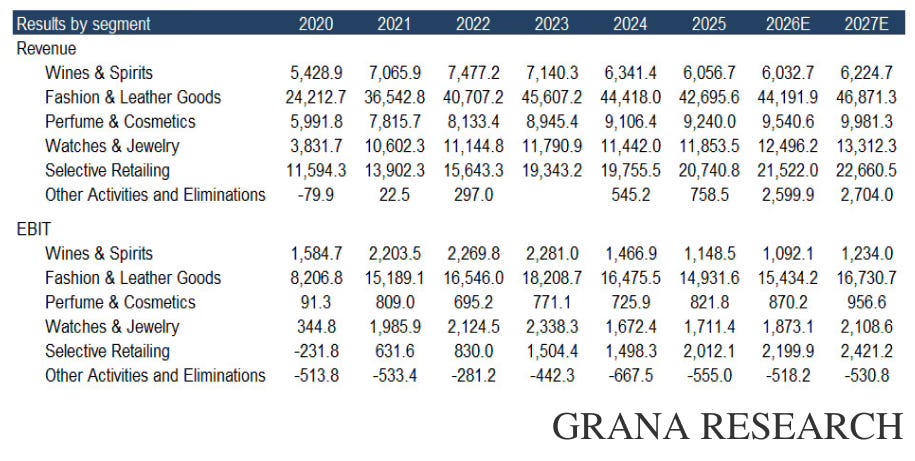

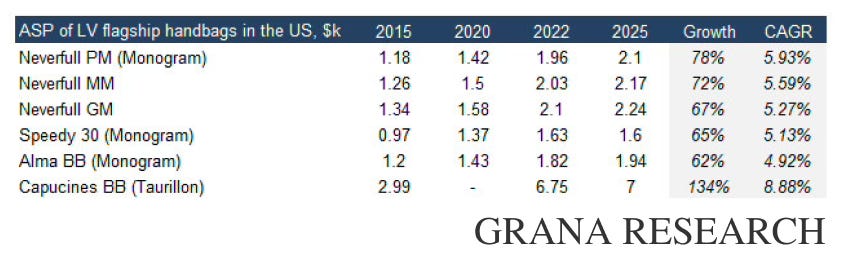

The Louis Vuitton brand has historically enjoyed strong pricing power: a 5% increase in prices for key products — primarily iconic handbags — would theoretically add around 2% to segment revenue. This implies that handbags account for roughly 40% of Fashion & Leather Goods (F&LG) revenue. And the company has actively leveraged this.

The brand has for many years raised prices on its key models annually — and sometimes more frequently — reinforcing Louis Vuitton’s positioning as an ultra-luxury brand and supporting high residual values in the secondary market. In 2020-2022, LV implemented several notable rounds of price increases, but the pace of indexation has since slowed. Moreover, in recent earnings calls, C-level executives have placed unusually strong emphasis on maintaining price discipline. In effect, this suggests that Louis Vuitton has temporarily (though potentially for an extended period) lost one of its key revenue growth levers.

Here are several comments from Tegus insiders and analysts from client-only reports regarding the current situation:

“For the current luxury, the narrative is still spreading that luxury is a scam or people feel they are more [rational]. The whole luxury disenchantment movement is still ongoing and more and more people are believing that luxury is not something appealing or it’s not something they aspire to. I think, on the demand side, there’s not only income issue but also this narrative spreading on social media.” - Luxury Critic, Senior Editor at LADYMAX

“If you look at LV probably last year, massive increase in price. Bring new creative director. Increase the prices because they know they're going to do less volume just by nature of the business and hence, trying to offset their sales reduction or traffic or volume by the increase in price. Didn't work out.” Former CFO Americas, Fendi at LVMH

In our view, the situation is complex and has two sides:

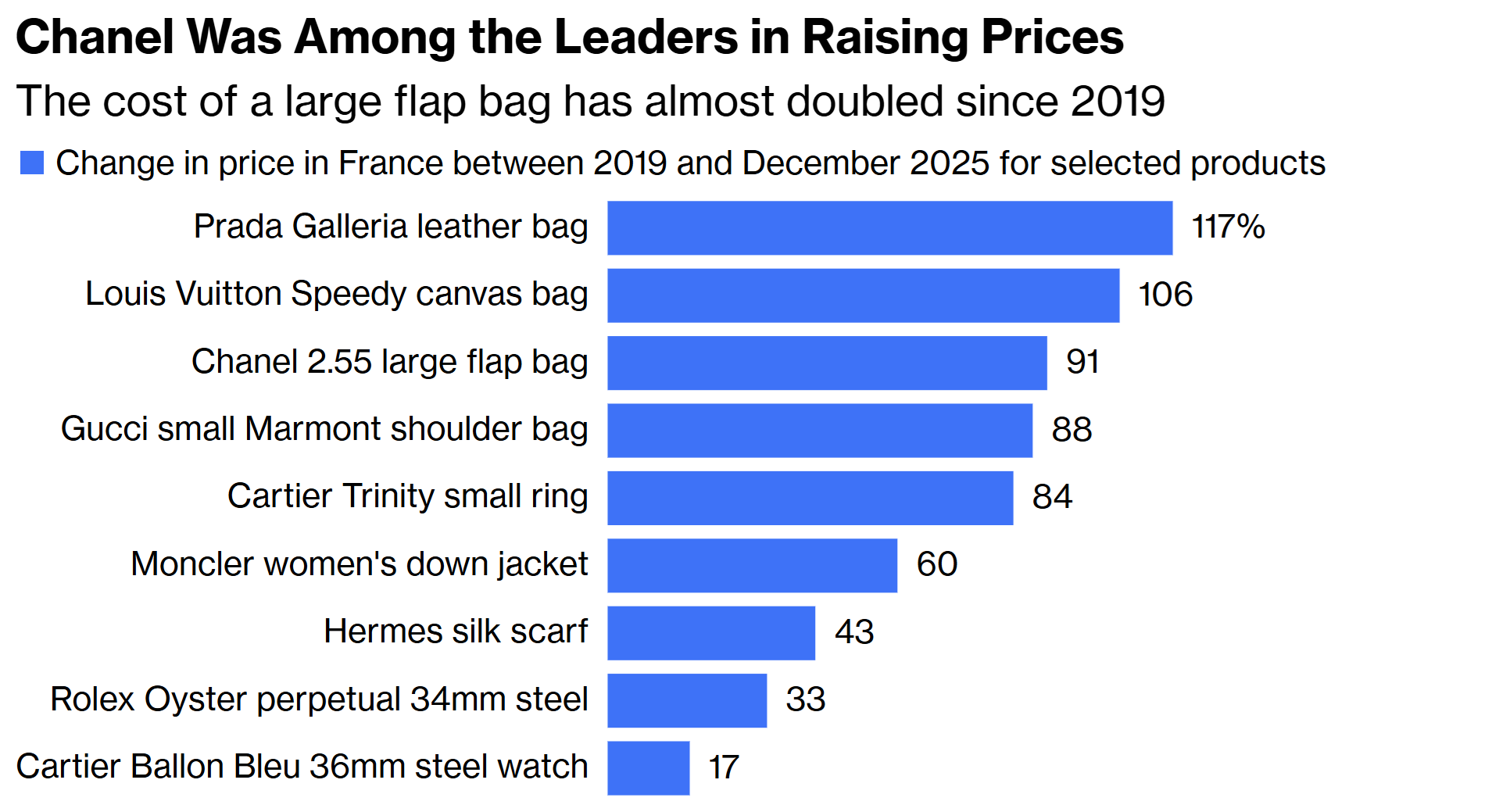

Negative: loss of part of the customer base due to resale and the risk of losing “desirability.” According to Bain & Company, spending on new luxury goods declined by 7% among Generation Z and by 2% among millennials in 2024. “Appetite for these brands and products remains high, but the willingness to pay current prices is low,” says Claudia D’Arpizio, Global Head of Fashion & Luxury at Bain & Company. Against this backdrop, some consumers are shifting toward the secondary market. Among the most in-demand brands on resale platforms are Louis Vuitton, Chanel, and Gucci.

The secondhand luxury market is estimated at $56 billion — nearly three times larger than a decade ago. Increasingly, consumers check resale prices before purchasing new items. For brands with strong residual value (such as Louis Vuitton or Bottega Veneta), this is a positive: their bags retain on average 89% of their original price upon resale.

Brands are now actively using reseller data to track demand. For example, the price of Chloé Paddington bags on The RealReal increased from $217 in 2024 to $724 in 2025, prompting the brand to quickly reissue the model. Louis Vuitton and Balenciaga have also revived archival designs. For some LVMH brands, this serves as an additional marketing resource, but in the event of declining “desirability,” the situation could change dramatically. This could lead to an accelerated migration of customers toward resale, other brands, and even counterfeits.

“Even for some well-educated people, they’re opening to buy takedown version of luxury or even counterfeit… People don’t have luxury shame. A lot of people, they are very close. They will disclose they wear counterfeit and the genuine products at the same time.” - Luxury Critic, Senior Editor at LADYMAX

Positive: the emergence of more affordable products and, as a result, a larger total addressable market (TAM). LV is actively lowering the entry price point into the brand, which may attract new customers:

“The entry ticket in order to have something originally from Vuitton was very expensive. Now there was a change in strategy in Vuitton. I would say most luxury brands, they started to develop wallets, shoes, tennis shoes. There is some people wearing Vuitton because they buy a $1,000 tennis shoes and it’s an original Vuitton tennis shoes. That’s in my perspective the way they are approaching younger generations or lower segment of income, that’s one way, by the average selling price of the ticket”. - CFO at LVMH

At present, Louis Vuitton is effectively serving as a platform for testing new retail formats and expanding its product matrix — which appears risky, given that the brand is also the primary engine of the entire conglomerate. The company is trying to sit on two chairs at once: to preserve a sense of exclusivity while simultaneously driving sales through more accessible products and a softer pricing policy. This likely implies more moderate annual price increases and the development of entry-level categories, particularly small leather goods.

However, this ambiguity dilutes the brand’s positioning and makes it harder to compete with brands where pricing logic and the perception of scarcity remain crystal clear to customers — such as Hermès and Chanel.

Creative Directors vs. Creative Direction

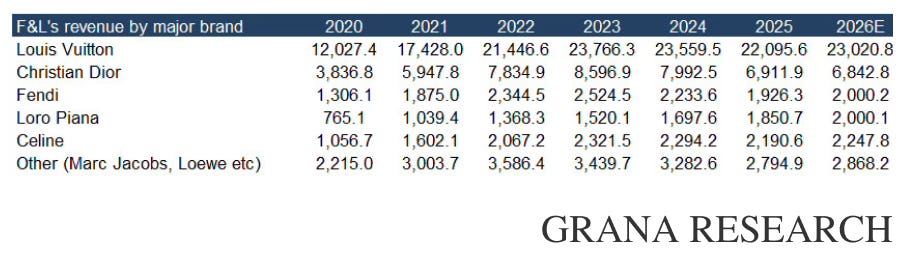

In fashion, the creative director is effectively the architect of product strategy, the cadence of novelty, and the codes a brand will commercialize. This season has been one of the richest in fashion history in terms of leadership reshuffles. Following the debut of Matthieu Blazy as Creative Director of Chanel at Paris Fashion Week, perhaps the second most significant event was the appointment of Jonathan Anderson at Dior (the second-largest brand within the LVMH Moët Hennessy portfolio by revenue after Louis Vuitton).

In a positive scenario, analysts compare the current situation to the late 1990s, when John Galliano, Alexander McQueen, Nicolas Ghesquière, and Martin Margiela fundamentally reshaped fashion and pop culture, successfully balancing creative innovation with commercial success. Chanel and Dior appear to be potential beneficiaries of this industry “reset,” while some players risk losing market share, according to Bloomberg.

As noted by The Business of Fashion, a strong start is crucial for brands today: early signs of success can help regain consumer attention and trust, but the effectiveness of these changes can only be assessed after several seasons. Dior’s transition under Anderson is a calculated risk. The scale of the brand is enormous, but his experience at Loewe increases the likelihood of a successful transformation, even if it takes time. Most of his products will only be available in stores toward the end of this year, and the full impact of his appointment will likely become clear only by mid-2026.

To better understand the situation, we decided to draw parallels between Dior’s two most recent creative directors:

Maria Grazia Chiuri (Womenswear): 2016-2024

Under Chiuri, Dior’s revenue increased more than fourfold. Her “perpetually safe” Dior was not considered particularly exciting by the niche fashion community and was often criticized for a lack of edge and creative boldness. However, it was crystal clear to the core base of affluent female clients — and therefore commercially highly successful.

So why was there a need to part ways with Chiuri? Prices for luxury goods continue to rise, which means that either product quality (where Dior remains strong as a largely craftsmanship-driven brand) or creative direction must evolve — otherwise consumers will simply turn away. Under her tenure, there was a growing sense of narrative fatigue: audiences were craving something new and exciting. As a result, conglomerates across the industry are increasingly embracing change.

“There has also been a significant amount of bad press surrounding the cost of labor and materials to create some coveted luxury goods vs. the retail markup… turning customers off”. - Former Manager, Media & Digital (Van Cleef & Arpels)

“There’s a shift towards commercial luxury items and concerns about lack of newness… I think it was because the artistic director was the same. It really started because of the product strategy. They just introduced the right product at the right time [before], but now that’s missing”. - Former Head of Sales - Europe & Middle East at LVMH

“Dior must reinvent the experience and find a way to surprise again and again their customers…” - Former Visual Merchandising Director — EMEA at Christian Dior Couture (29 Apr 2025)

Jonathan Anderson: 2025-Present

The first designer since Christian Dior himself to simultaneously oversee all divisions of the house — menswear, womenswear, couture, and accessories. At least, this is how Anderson is presented by the Arnault family; formally, a similar level of authority was once held by Marc Bohan. In any case, the responsibility is enormous. The pressure is immense — especially considering how much LVMH Moët Hennessy has monetized Dior’s womenswear division under his predecessor.

Anderson must attract a new audience without alienating the existing one:

“You can’t assume that even if you lose one existing client, you will simply gain two new ones thanks to unique creative solutions. The days when you could join a brand and start from a blank slate are over,” - Robert Williams, an editor at The Business of Fashion specializing in luxury brands

Anderson is a driven art enthusiast, long favored by a similarly niche or aspirational audience. He has successfully managed both his eponymous brand, JW Anderson, and Loewe. Under his leadership, Loewe’s revenue grew over 11 years from approximately €230 million to €1.5–2 billion. However, Jonathan is now compelled — and intends — to appeal to a much broader audience. Will it work? We will see. That said, sentiment among observers and insiders regarding Anderson’s era at Dior is generally bullish:

“I think that Dior will probably gain market shares. LOEWE has been, so far, a very desired brand… They were leading the luxury arena when JW Anderson was at the helm of the creative direction of LOEWE. I think this is going to be the case for Dior. The industry, and probably, all the clients of the luxury industry are waiting to see its first collections hitting the stores.” - Global Head of Sales Merchandising - Ready-to-Wear at Chloé

“He does have a great track record. I think what he did at Loewe was incredible. It was an unknown name to a very strong player in the industry… it’s really interesting and the right move that they have him overseeing both men’s and women’s, because I think from a brand direction perspective, it’s always been so disconnected… To bring it all under one designer again for the first time since Christian Dior himself, that is a big, bold move.” - Former Senior Director, West at Dior

“He has a very strong point of view on what the luxury market should be… He takes a point of view from a different generation… He has a very sharp point of view on what are the codes that a luxury maison should be using today to be relevant with that Gen Z cohort of people.” - Former Brand President, North America at Bulgari

There are already some early positive signals. Jonathan Anderson’s first womenswear collection at Dior became the second most viewed Spring/Summer 2026 collection on Vogue Runway, уступив лишь дебютной коллекции Matthieu Blazy at Chanel.

Anderson did exactly what the market was expecting: he engaged with the house’s core codes. While the Bar jacket was not radically reinterpreted, the key accessory — the Lady Dior — underwent a meaningful “reboot.” The bag remained rooted in Dior’s DNA but evolved in form: softer versions emerged, alongside new materials and unconventional proportions. This was critically important.

Across Tegus materials and public sources, there has been a consistent narrative around the lack of new strong product hits, particularly in leather goods. Insiders pointed to the exhaustion of flagship lines, a limited set of products capable of consistently driving turnover, and growing consumer fatigue with logomania:

“There has really not been any innovation in product in the last six or seven years… there is a finite amount of Lady Diors and Book Totes and Saddle Bags that are going to drive your business, especially as you get to this $1+ billion mark.” - Former Senior Director, West at Christian Dior Couture (30 Jul 2025)

At Louis Vuitton, creative leadership is split between two figures: Nicolas Ghesquière (womenswear) and Pharrell Williams (menswear). This has created a structural setup the brand has not encountered in this form before, and it carries a number of implications:

A split in the brand’s visual and stylistic codes. The menswear line, following the arrival of Pharrell Williams, has taken on a bold, pop-cultural direction — collaborations, media visibility, streetwear influence, and strong resonance on social media. He has revitalized men’s Louis Vuitton, making it more visible and desirable. Meanwhile, the womenswear collections under Nicolas Ghesquière are increasingly perceived as somewhat dated and predictable. His approach leans toward a refined but expected aesthetic, which experts often describe as “redundant” and “lacking innovation.”

A divergence in commercialization. The menswear segment — particularly ready-to-wear — benefits from the buzz surrounding Pharrell, whereas the womenswear division, which remains the key revenue driver, lacks a comparable creative “spark.” This creates an imbalance: the brand is perceived as highly “hot” in menswear from a media standpoint, yet financially it remains dependent on the more conservative womenswear segment.

Complexity in product strategy and communication. Two creative teams with different approaches are producing collections, campaigns, and collaborations with distinct aesthetics. This makes it more difficult to build a cohesive narrative in global marketing campaigns — especially in Asia, where consumers are particularly sensitive to a unified “brand image.”

Risk of audience fragmentation. The menswear line is more successful in attracting a younger and broader audience, while womenswear remains focused on traditional HNW clients. Without alignment in positioning, the brand risks being perceived as two parallel worlds rather than a single, unified Louis Vuitton house.

Here are several insider comments on the current situation:

“If I think about Vuitton internally, they have Pietro Beccari — he's fantastic. From a leadership perspective, Pietro has been able to move them forward and resolve internal challenges. Obviously, the appointment of Pharrell Williams was really interesting and made a lot of waves in the menswear space, which you have to do when you're a luxury player in that segment.” - Former Senior Director, West at Christian Dior Couture

“Even if we think of Louis Vuitton, they still have two different creative directors. They have Nicolas Ghesquière for the women's universe and Pharrell for men's, but they still rely on two separate creative directors, which is quite a challenge because sometimes we see a gap between the women's and men's categories. From my perspective, Pharrell has made the men’s universe very, very attractive. Nicolas Ghesquière has been at the helm of womenswear for such a long time — it feels very redundant and lacking innovation. This is probably what disappoints many of the brand’s clients. Again, in tough markets like Asia, a lack of innovation is a major challenge.” - Global Head of Sales Merchandising – Ready-to-Wear at Chloé

At present, there is no publicly available or insider information regarding potential changes to the creative director roles at Louis Vuitton.

Catching a “Wolf in Cashmere” by the Tail

The internal dynamics within Bernard Arnault's family are increasingly being compared to the plot of the TV series Succession: all five of his children are involved in managing LVMH Moët Hennessy and are competing for influence within the group. A de facto “Darwinian” model has formed within the company, with competition for positions and a gradual selection of a potential successor. While the market may tolerate uncertainty around succession as long as the business is growing rapidly, in a phase of “normalization” or stagnation, any managerial uncertainty becomes significantly more costly.

Children from the first marriage (with Anne Dewavrin):

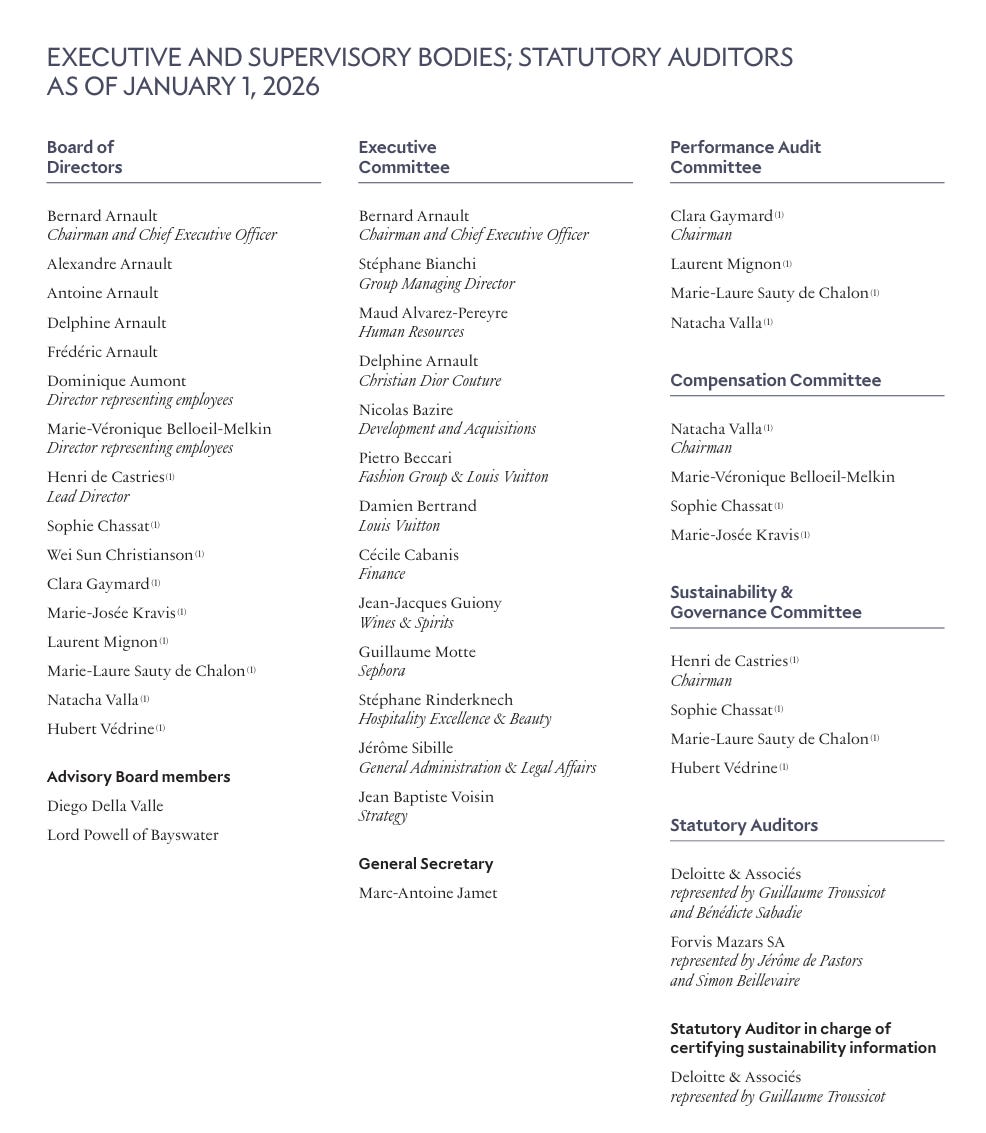

Delphine Arnault — the eldest daughter. Since February 1, 2023, Delphine Arnault has been Chairman and Chief Executive Officer of Christian Dior Couture. She is a member of the LVMH Board of Directors and the Executive Committee.

Antoine Arnault — Director of Image & Environment, also a member of the Executive Committee; Chief Executive Officer and Vice-Chairman of the Board of Directors of Christian Dior SE.

Children from the second marriage (with Hélène Mercier):

Alexandre Arnault — one of the younger sons, Deputy Chief Executive Officer of Moët Hennessy, and a member of the LVMH Board of Directors. Previously Executive Vice President at Tiffany & Co.

Frédéric Arnault — Chief Executive Officer of Loro Piana; previously CEO of TAG Heuer and head of LVMH’s watchmaking division.

Jean Arnault — Director of Marketing and Development for Louis Vuitton Watches, overseeing the brand’s watchmaking activities.

Here’s what matters:

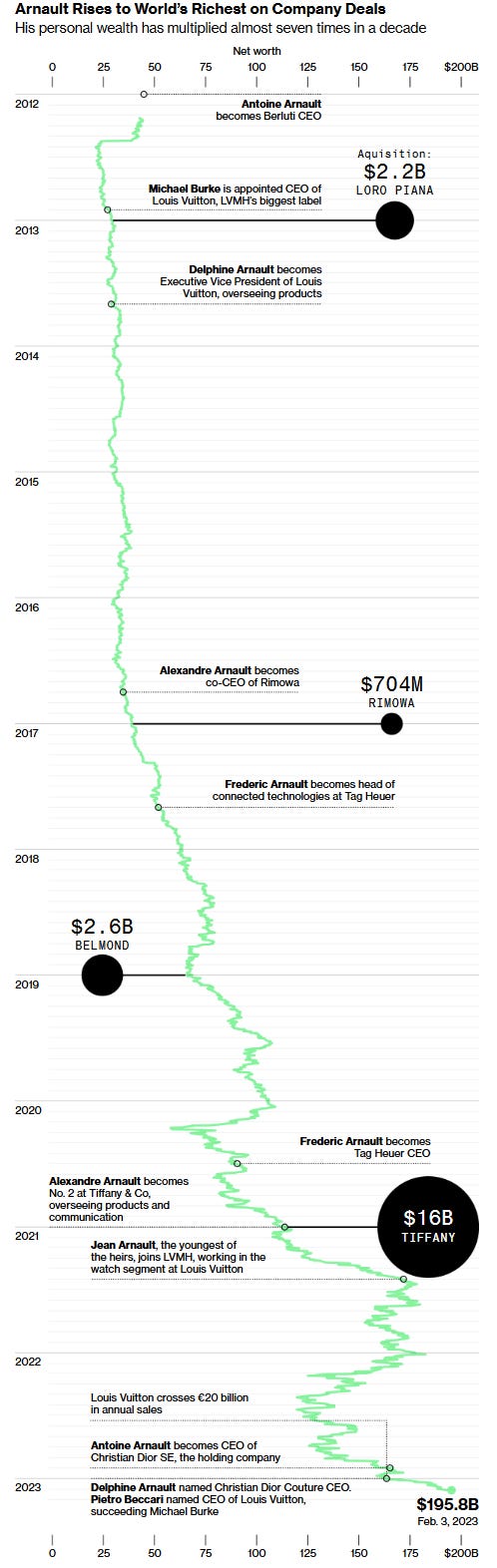

Shareholders approved a change to the company’s bylaws allowing Bernard Arnault to remain Chairman and CEO until the age of 85. The decision was supported by 99.18% of votes. The age limit had previously already been raised — from 75 to 80 in 2022. Arnault, now 77, continues to combine the roles of CEO, Chairman, and controlling shareholder of LVMH Moët Hennessy.

The family has strengthened its control. In February 2026, regulatory disclosures showed that the Arnault holding structure crossed the 50% ownership threshold (50.01%). This is symbolically important: an absolute majority stake reinforces the family’s “defensive shield” against external pressure.

The extension of Bernard Arnault’s tenure to age 85 reduces near-term uncertainty. However, the succession question remains open and acute: this is more a postponement of the decision than a resolution. Shareholders of LVMH Moët Hennessy are increasing pressure on the company, demanding greater transparency on this issue. A concrete succession plan has still not been disclosed, and any changes at the senior management level continue to fuel speculation about a potential distribution of roles within the family.

The governance structure reinforces this dynamic. All heirs are regularly involved in strategic discussions — Bernard Arnault holds monthly meetings with them — and the market interprets key appointments as signals of the balance of power within the family. At the same time, control is evenly distributed: each of the children holds an equal stake in the holding structure that is expected to assume control after Arnault steps down.

The family’s key holding structures include Financière Agache and Agache. Following the 2022 reorganization, all five heirs — Delphine Arnault, Antoine Arnault, Alexandre Arnault, Frédéric Arnault, and Jean Arnault — each hold a 20% stake in Agache Commandite SAS, which is set to control the family holding in the future. Corporate governance experts warn that such a structure increases the risk of disagreements in decision-making and may complicate the selection of a single leader.

The configuration of “centers of power” within the family/group can be clearly inferred from official appointments.

At the same time, even large institutional shareholders acknowledge that they have no clear understanding of how a potential transition of power would be structured. Moreover, the issue is hardly discussed within the family itself. Hélène Mercier, the wife of Bernard Arnault, stated in an interview with Libération that the topic is “almost never” raised and that the decision rests entirely with Arnault. Potential frictions among the heirs and the absence of a clear succession mechanism increase the likelihood of long-term governance risks and may be reflected in the company’s valuation through a discount to multiples.

So where does this leave us? Bernard Arnault is already 77 and has no intention of stepping down: he has extended his ability to remain CEO until 85 and has explicitly stated that the succession issue can be revisited “in 10 years.” This sets the baseline framework — formally, there is ample time, but the market perceives the situation differently. Investors are already citing the lack of a clear plan as a source of risk and opacity, which is beginning to weigh on the company’s valuation.

At the same time, the governance structure is designed so that all five children remain actively involved. They hold operational roles in key group assets — Dior, Moët Hennessy, Tiffany, and Loro Piana — and are not merely nominal heirs but active managers. Simultaneously, they each own equal stakes (20%) in the family structure that will ultimately control the holding, implying a model of collective decision-making. Against this backdrop, Arnault has been steadily increasing their presence at the center of governance. In 2026, Antoine Arnault joined the executive committee — the inner circle where key decisions are made — becoming the second family representative in that body after Delphine Arnault.

In our view, he is the most likely successor to the “wolf in cashmere.”